A $36T Problem

Elon Musk, DOGE, Dedollarization and the ballooning US public debt.

After the 2024 US Election that saw Donald Trump winning the presidency, the political involvement of his main supporter - Elon Musk - appears to be on the rise. Elon will co-lead "DOGE" or "Department Of Government Efficiency" with Vivek Ramaswamy. Despite the name, it's not an official Department of the US Government with executive powers, but rather a Presidential Advisory Commission intended to help the government reduce wasteful spending and improve budget efficiency.

The appointment of two successful entrepreneurs to these roles seems logical, and the reasoning extends beyond their support for Trump's campaign. Elon Musk, in particular, is well known for his obsession with cost reduction in his companies and his careful evaluation of potential returns on his investments. The most prominent example was an approximately 80% workforce reduction after the acquisition of Twitter, now X, without any visible negative impact on operations or the product. While the case initially sparked controversy, it effectively demonstrated that companies can be much more strategic in their resource allocation, to say the least.

The same principle applies to public organizations like the government, perhaps even more so, according to Musk. In many of his recent X posts, he has criticized several public projects and initiatives that - in his view - are expensive and unnecessary, and should be cut accordingly.

1. Why now and why it truly matters

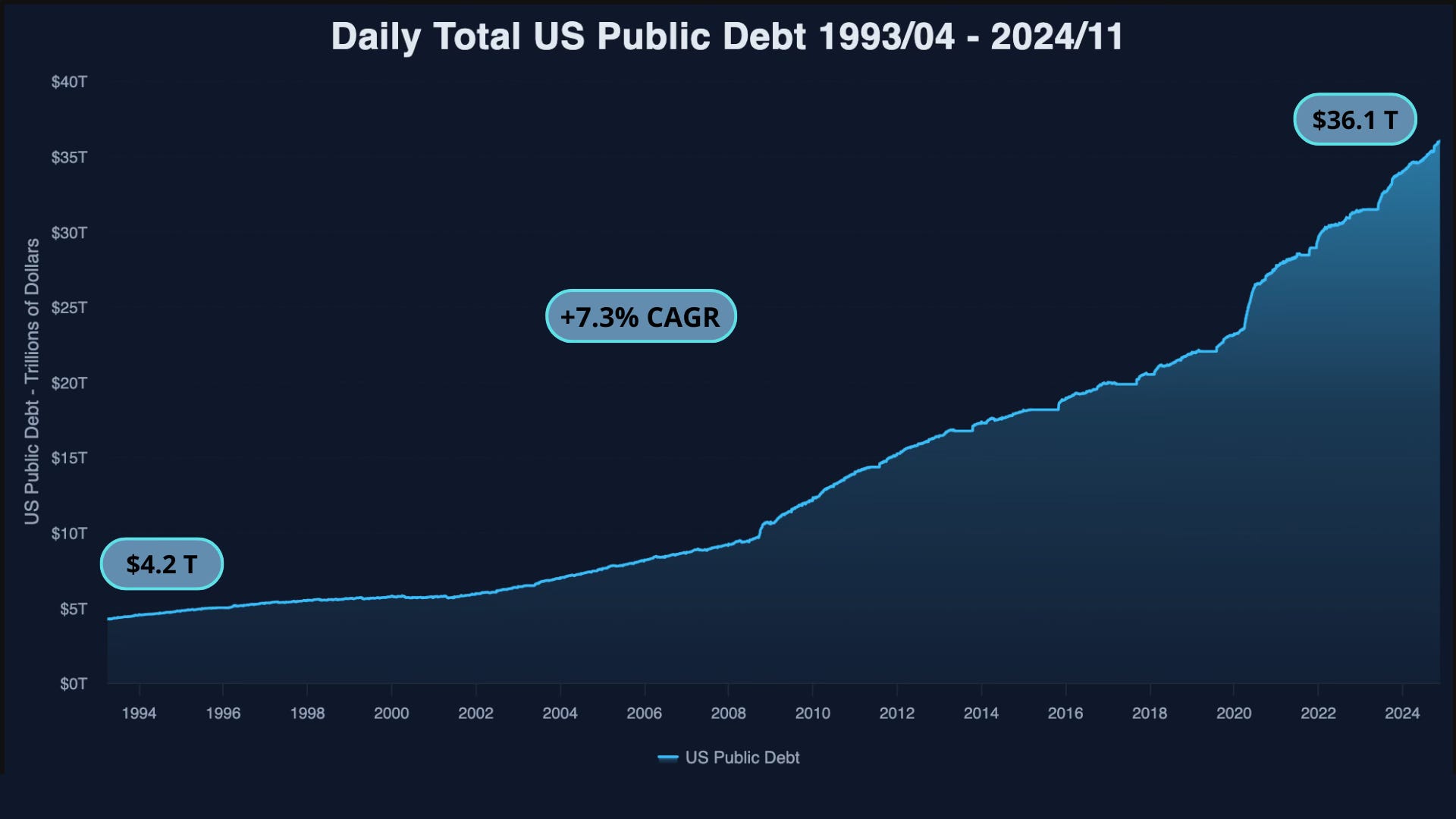

Long story short: the US Government has a debt problem. A big one.

Current US public debt stands at it’s all time high at over $36 Trillion, and is growing at an ultra fast pace, over $163.7B per month on average in the last year.

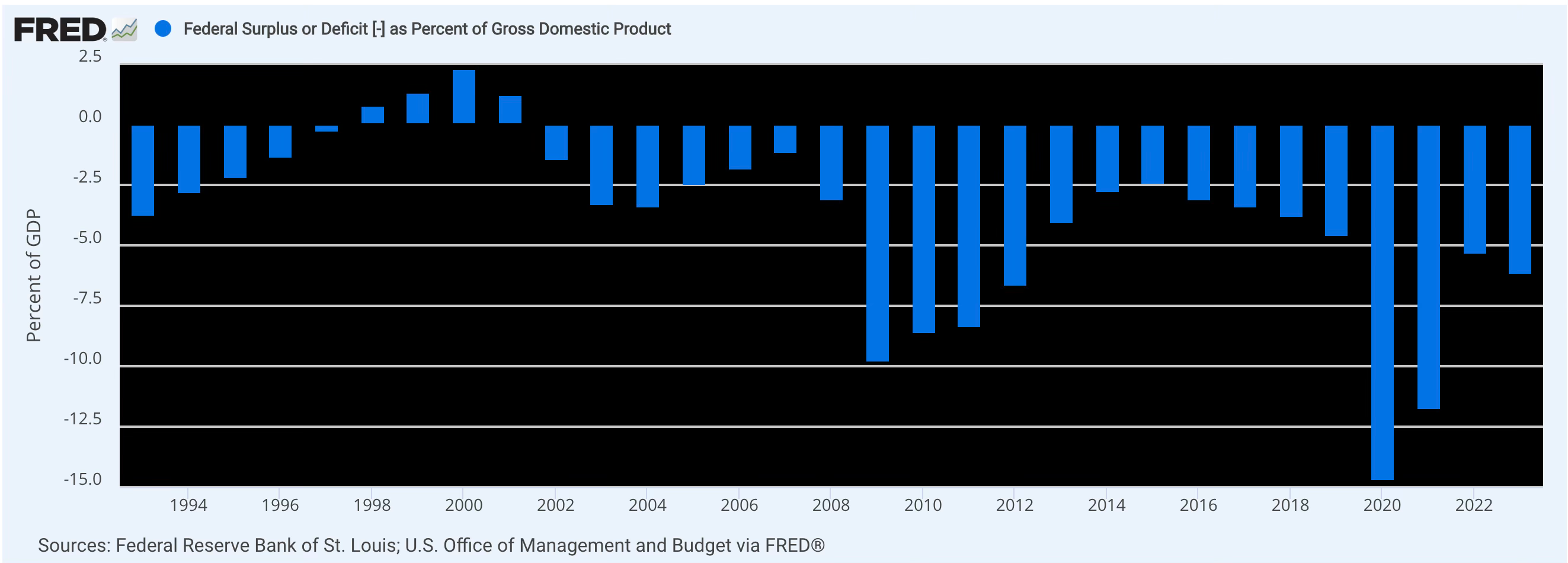

This is due to large budget deficits occurring almost every year since the early 2000s, which are not expected to diminish anytime soon, with the most recent forecasts from the Congressional Budget Office of ~6% of annual deficits in the next decade, reaching 7% in 2034.

Total debt is calculated as the sum of "Debt held by the public" and "Intragovernmental Holdings". The former should be considered "the real debt," which is debt issued to public and private investors who fund government spending, while the latter represents "money that the government owes to itself", such as imbalances between different states and the federal government. Therefore, we can focus solely on Debt Held by the Public and ignore the ~$7.35T of Intragovernmental Holdings. The US Public Debt currently stands at approximately ~$28.73T at the time of writing.

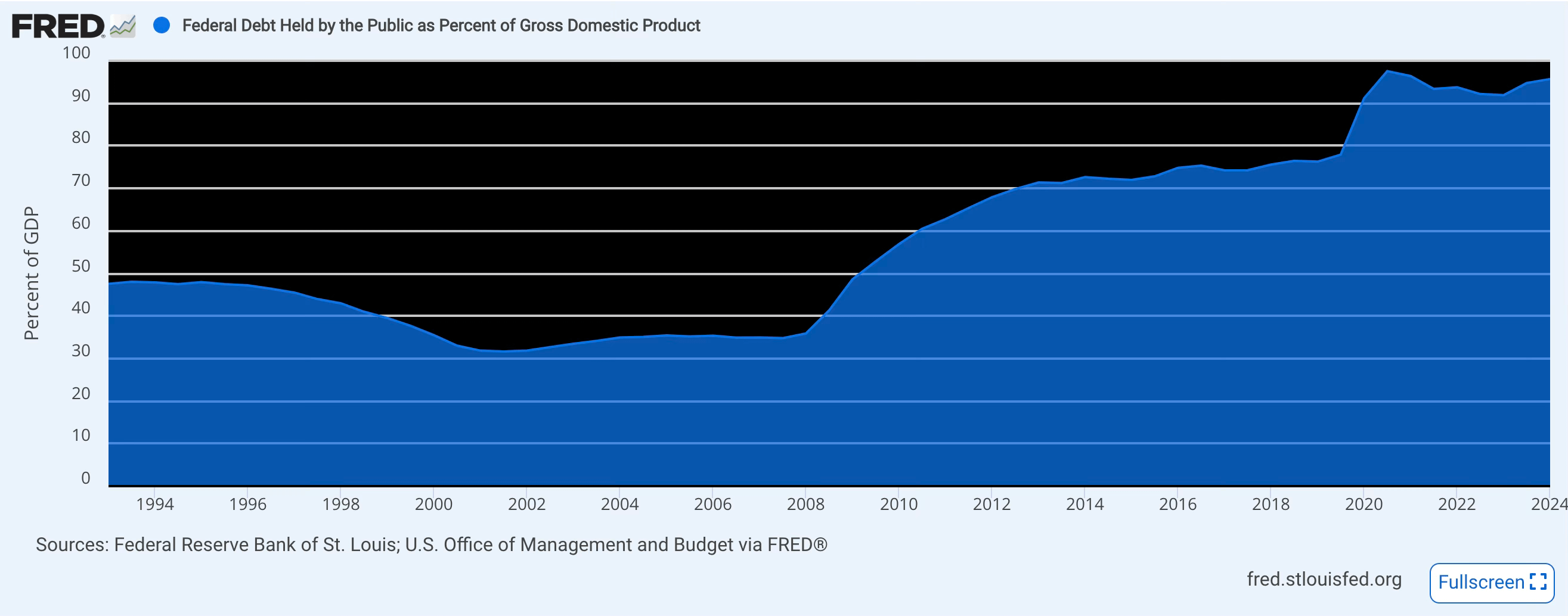

One might argue that the right way to view this is by looking at Debt as a percentage of GDP, but this perspective might be even more concerning.

The debt stands at around 100% of GDP. The latest data released by FRED (96.2%) refer to Q2 2024, but since then, the debt has continued to grow at a faster pace than even the most optimistic GDP forecast for the current year.

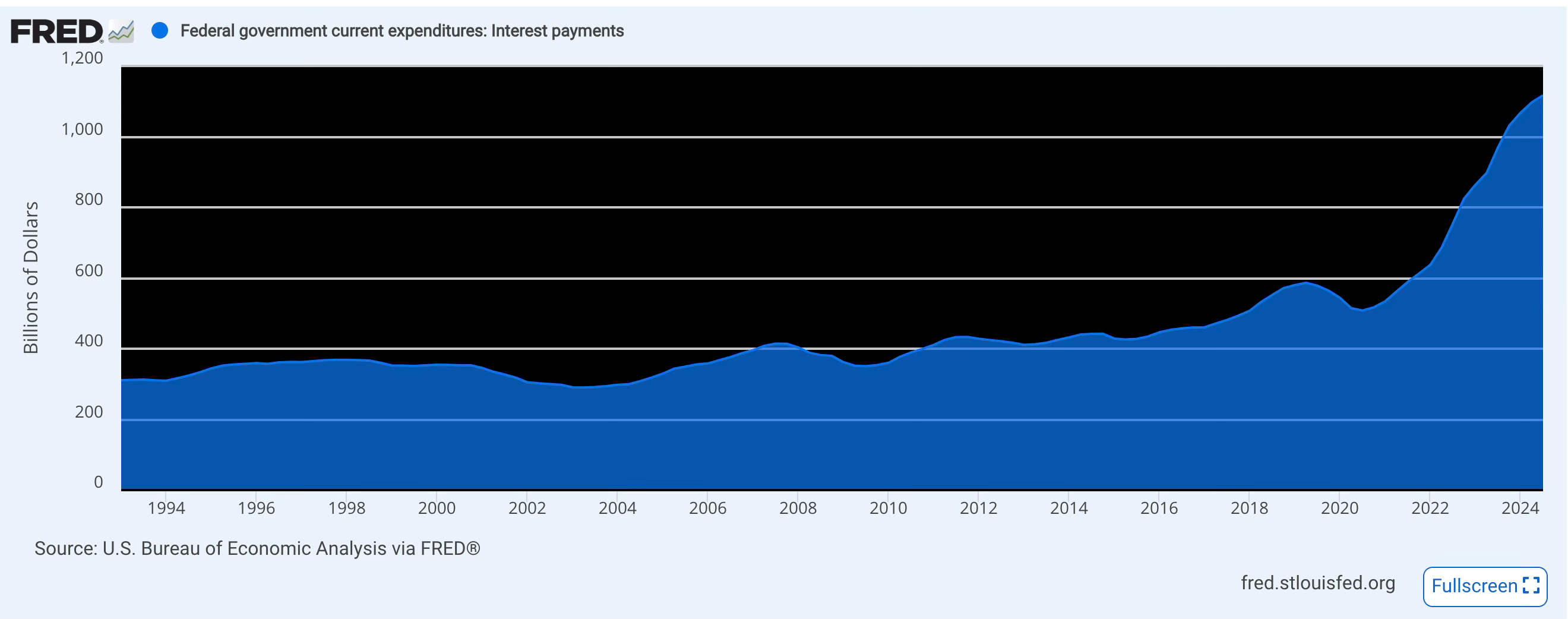

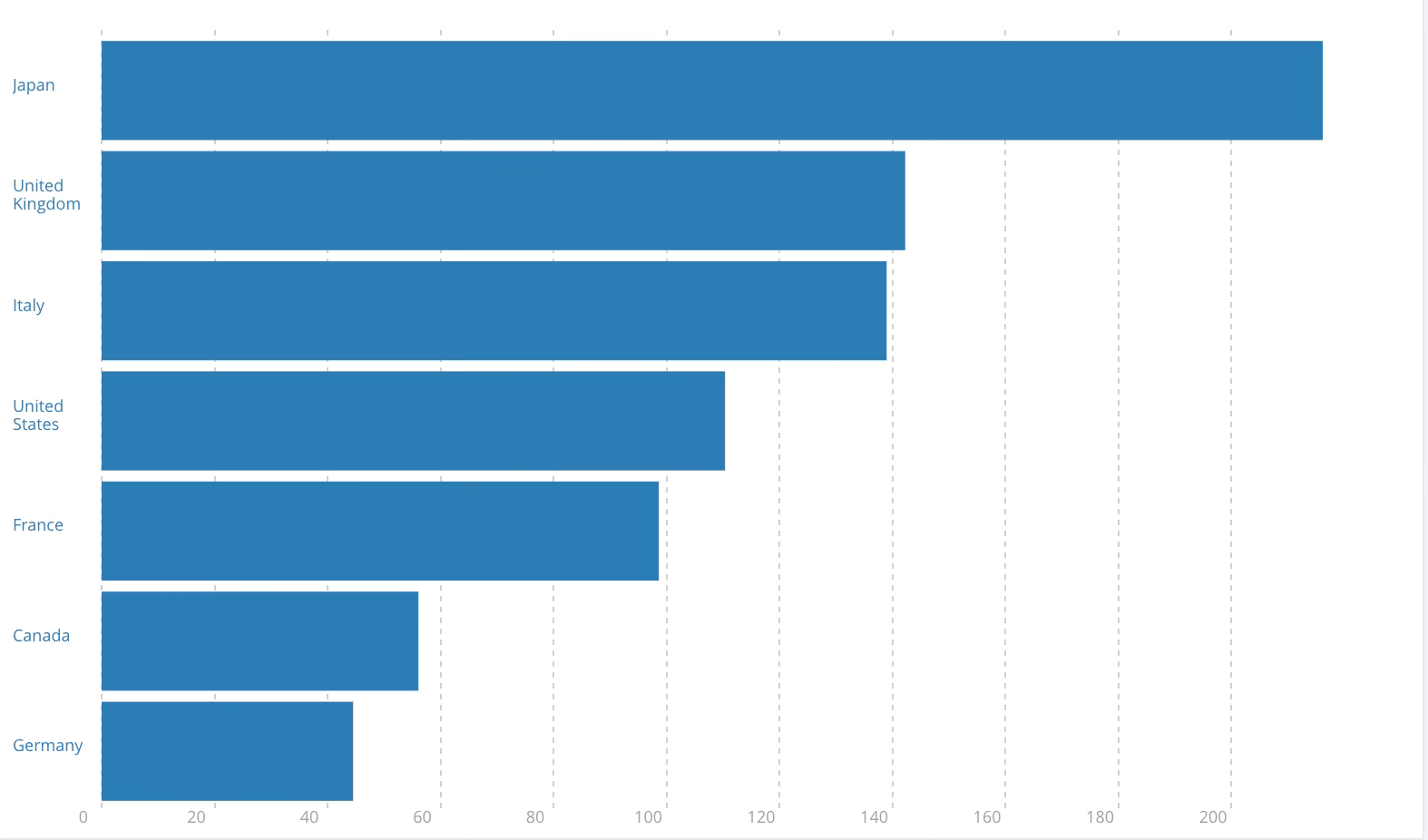

An additional challenge is the rise in interest rates - or cost of debt - over the last couple of years. After a long period of record-low rates, the Fed was forced to substantially raise the base rate in an attempt to curb inflation.

It's noteworthy that despite the Fed's 2024 rate cuts, the 10-year Treasury yield continues to hover around its 15-year high, with investors demanding a premium to compensate for inflation that is expected to remain above the Central Bank's target for an extended period. Considering that public expenditure contributes to higher inflation through increased demand for goods and services, and that higher inflation leads investors to demand higher interest rates regardless of Fed's cuts, it becomes clear that monetary easing efforts alone cannot break this cycle.

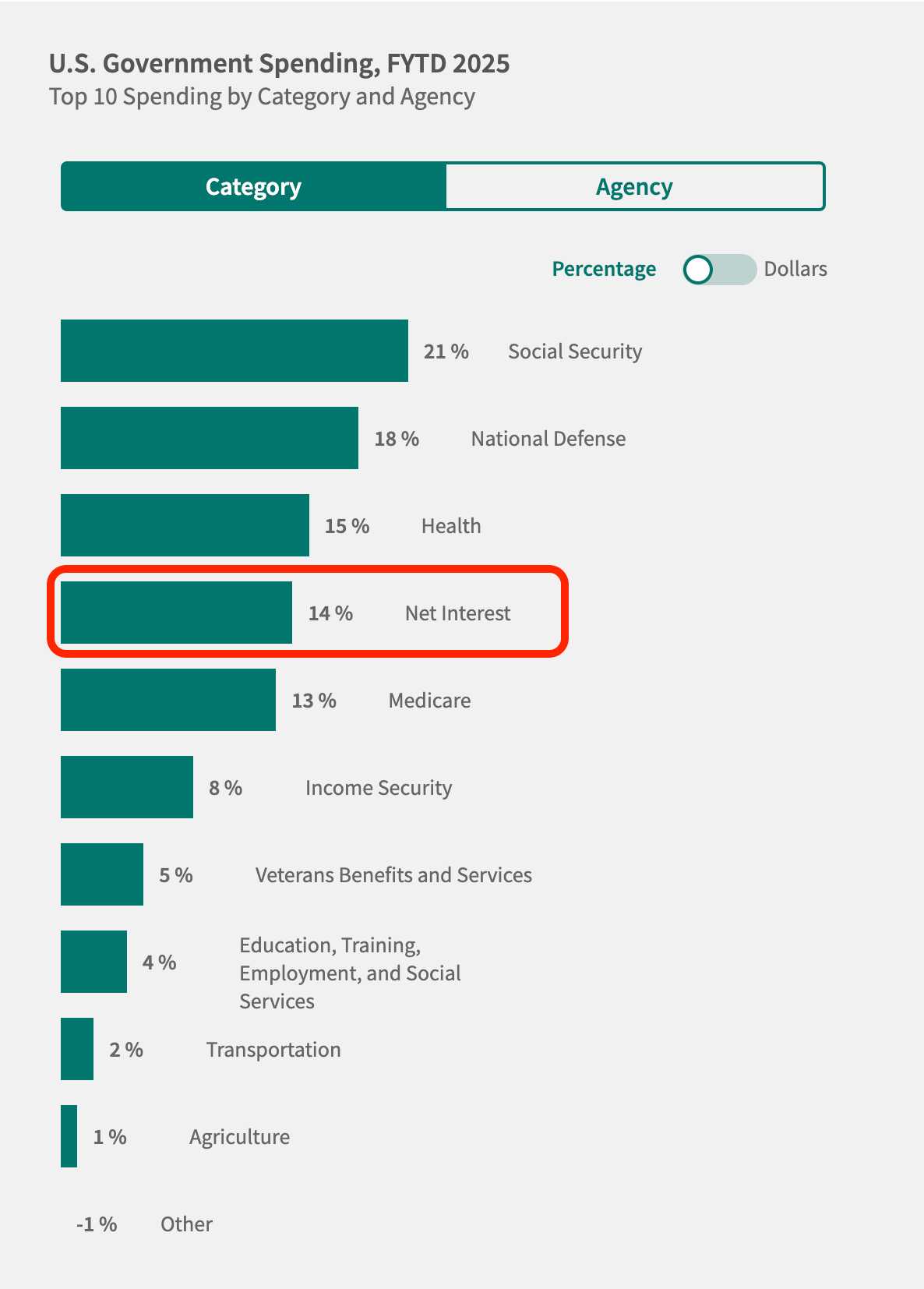

This spike in interest rates, combined with higher debt levels, has led to - predictably - a rapid increase in interest spending:

Now the expense on debt interest is one of the largest in the entire budget, and it continues to climb the rankings ($1.1T in last year).

This represents a heavy burden for future generations and governments, making it even more difficult to reduce the deficit in coming years.

2. The break point

Is there a point when debt becomes truly unsustainable? For over a century, we've been warned that public debt is "a time bomb," a serious problem requiring urgent attention, yet here we are, with the economy having performed well in the long term, even in real terms. So why should this time be different?

Well, the answer is rather subtle.

The entirety of US Debt is issued in US Dollars, so technically there isn't a point at which the Government would be forced to declare default - the inability to repay its debt - since the Fed could theoretically issue all the money supply needed for immediate repayment. However, this would trigger unprecedented inflation at such a scale that it would seriously undermine the economy for decades, if not longer. It would be like killing a patient while trying to cure the disease. Not exactly a solution.

Here’s the common formula to calculate the sustainability of debt:

The primary balance represents the fiscal deficit excluding the interest expenditure.

Replacing with 2024 US Forecast from IMF:

In other words, the debt-to-GDP ratio will grow by +4.2% in a single year!

There are thus two ways to reduce the debt-to-GDP ratio: reduce the debt by repaying it year by year, or increase GDP at a faster pace than the debt grows. However, these two approaches are closely interconnected: to repay the debt, you first need to have a surplus, which means reducing expenses and increasing tax revenues. But drastically cutting investments and public spending while sharply increasing taxes would inevitably impact GDP, possibly triggering a recession. On the other hand, stimulating the economy would require increased spending and likely lead to higher inflation, resulting in larger deficits and higher interest rates.

So, what’s the solution?

3. Here comes DOGE

According to Musk, the problem is not how much you spend how you spend.

This has been mostly ignored by most governments from long time, especially in the western world. A gradual increase in social spending and other voices without questioning what would be the expected return has led to a constant increase of debt without a proportional return on GDP.

In other words, is like a household borrowing money, regardless of its cost, for amenities and personal consumption and for many years instead of an entrepreneur asking for a loan to start a business. In the latter case it might seems risky, but over the long and spreading the sum in many different projects with care it may become sustainable. In the former case, the loss - or the bankrupt - is simply guaranteed.

In business terms, Musk aims to eliminate a long list of expenses with low - or even negative - ROI that aren't strategically important for the United States, while maintaining extensive government spending in areas that generate the most economic value.

Unfortunately, specific details about which areas would be impacted and the potential effectiveness of these measures remain unclear. We can only make educated guesses based on Musk's public statements, which have highlighted concerns about an excessive number of Federal Agencies and an oversized federal workforce. He has also criticized wasteful foreign aid spending and overregulation, which he argues creates costs for both the government and businesses that must comply.

Potential conflicts of interest are evident here, as Musk has repeatedly highlighted how stringent regulations have slowed down his own businesses - SpaceX, Tesla, and The Boring Company - while forcing higher expenditures than planned. Undoubtedly, Elon's first venture into public service will attract significant scrutiny.

4. Dedollarisation - What’s the connection?

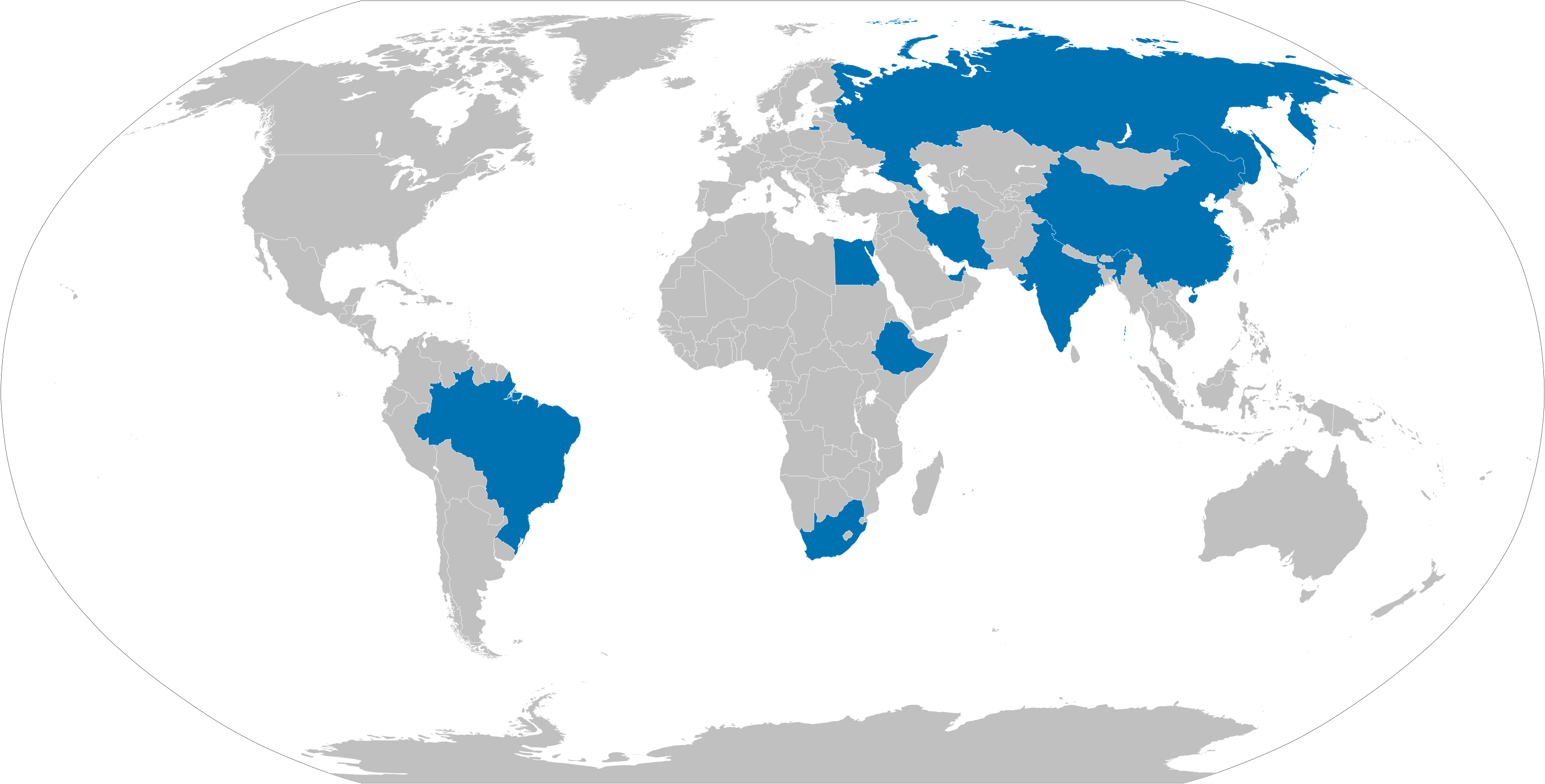

In recent years, there has been a surge in discussions about "de-dollarization" - the gradual effort to reduce the global role of the US Dollar in international trade and as a means of financial stability for Central Banks worldwide. These efforts are led by the BRICS nations - especially Russia and China - and have accelerated following international sanctions on Russia after its invasion of Ukraine. However, many other countries worldwide, including US allies, have shown serious interest in this approach.

Some initial steps in this direction are already visible, with Russia trading natural gas and oil with China exclusively in Chinese Renminbi and Russian Rubles, while other countries such as India and Saudi Arabia are accepting and executing at least part of their payments in currencies other than the American dollar.

Most coverage of de-dollarization has so far focused primarily on the political objectives of America's global adversaries, who seek to avoid sanctions, prevent potential leverage over their governments, and aim to financially weaken the United States.

That's only part of the truth. There are also profound economic implications of relying so heavily on another country's currency. For instance, there's a risk that the Fed might supply large quantities of money into the system to support the debt while tolerating higher levels of inflation to bolster the American economy. This would gradually weaken the real value of the currency, thereby harming countries with large USD reserves. These countries, particularly major commodity exporters, would experience a constant erosion of the real value of their USD reserves while being forced to maintain them for trade with their partners.

It comes as no surprise that countries like the UAE and Iran joined the BRICS in 2024. Saudi Arabia, the world's largest crude oil exporter, planned to join the group and only halted the process after strong pressure from the USA, though it continues to consider the matter. Notably, all members of the enlarged BRICS are heavily involved in commodities trading, which is currently conducted in dollars.

When the Federal Reserve issues large quantities of dollars, it spreads the burden of inflation among all dollar holders worldwide, while the benefits of such issuance accrue exclusively to the United States. The current state of US finances, extreme budget deficits, and rising debt levels are pressuring nations to consider de-dollarization as a realistic option for their future, even those that previously had no interest in pursuing such a direction.

Given the dollar's global dominance, the process would likely take decades to complete, assuming it ever reaches full realization. However, American government policies can dramatically accelerate or slow down these efforts, depending on how seriously it commits to achieving a more solid financial position.